Financing a boat doesn't have to drain your savings or lock you into sky-high monthly payments. Whether you're eyeing a traditional vessel or a compact electric watercraft like a Wave-Vo, low interest boat loans can make ownership far more accessible. The key is knowing where to look, and what terms actually benefit you versus the lender.

Interest rates on marine loans vary wildly depending on the lender, your credit profile, and the type of boat you're purchasing. Some banks offer rates as low as 5.99% APR for qualified buyers, while others quietly tack on fees that inflate your total cost. This guide breaks down 12 lenders worth considering in 2026, with transparent comparisons of their rates, terms, and approval requirements.

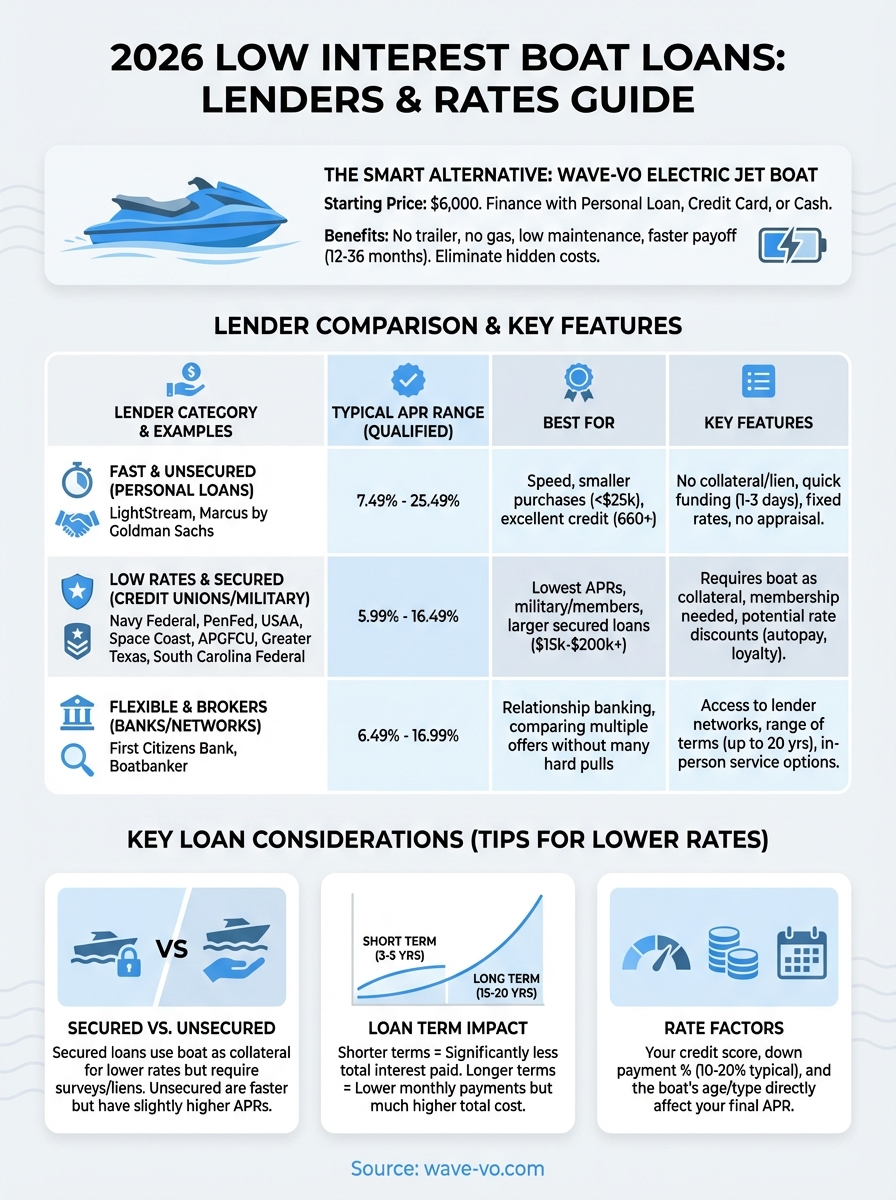

At Wave-Vo, we built our electric jet boats to eliminate the traditional headaches of watercraft ownership, no trailer, no gas, no complex maintenance. But we also know that upfront cost still matters to most buyers. That's why we put together this resource: to help you find financing that fits your budget, whether you're buying one of our $6,000 electric jet boats or a larger vessel. Below, you'll find the lenders offering the most competitive rates this year, plus tips for locking in the lowest APR based on your situation.

1. Wave-Vo

Before you compare low interest boat loans, consider whether you actually need a five-figure loan at all. Wave-Vo's electric jet boats start at $6,000, which puts them in a price range you can cover with a personal loan, credit card, or even cash savings in many cases. Traditional boats and jet skis often push buyers toward long-term marine financing with lender-imposed requirements like surveys, insurance riders, and collateral inspections. You skip all of that when your watercraft costs less than a used sedan.

Why Wave-Vo can reduce your financing needs

Wave-Vo jet boats eliminate the hidden costs that inflate traditional boat ownership. You won't pay for trailer registration, gas dock trips, winterization services, or marine mechanic labor. The 15kW electric motor runs on a 5.5kWh battery you can swap in 10 seconds, and charging at home typically costs under $2 per full charge. Over five years, you'll avoid thousands in fuel and maintenance expenses that would otherwise require bigger monthly payments.

Most boat loans lock you into 10 to 20-year repayment schedules because the purchase price demands it. Wave-Vo's lower entry cost means you can pay off the balance in 12 to 36 months with a standard personal loan, saving you years of interest accumulation. That shorter timeline also protects your budget if your financial situation changes or you decide boating isn't for you after a season or two.

What it costs compared to traditional boats and PWCs

A new jet ski from major manufacturers costs $9,000 to $18,000 before dealer fees, while aluminum fishing boats with outboard motors start around $15,000 for basic models. Wave-Vo's $6,000 base price includes the hull, motor, battery, and charger. You'll pay shipping fees based on your location, but you avoid dealer markups, freight charges, and the $1,500 to $3,000 cost of a trailer since the 75kg hull fits inside most SUVs and pickup beds.

"When your watercraft costs less than a high-end laptop, you can finance it like consumer electronics instead of real estate."

When a small personal loan beats a long boat loan

Personal loans from lenders like LightStream or Marcus (covered below) offer fixed rates between 6% and 12% APR for qualified borrowers with good credit. If you borrow $6,000 at 8% APR over three years, your monthly payment lands around $188, and you'll pay roughly $770 in total interest. Compare that to a 15-year boat loan at 7% APR on a $25,000 vessel, where you'd pay over $11,000 in interest even at a lower rate.

Small personal loans also close faster. Most lenders fund within two to five business days, while marine-specific loans require appraisals and title work that can stretch approval to three weeks or more. You can order your Wave-Vo, secure funding, and be on the water in the same month.

What to confirm before buying and shipping in the US

Wave-Vo ships worldwide, but you'll want to verify delivery timelines and shipping costs for your specific ZIP code before finalizing your loan amount. The company provides a 1-year warranty and 14-day return policy, which matters if you're using a personal loan that doesn't have the same collateral protections as a secured marine loan. Check whether your homeowner's or renter's insurance covers watercraft up to $10,000 in value, or budget for a separate rider. Finally, confirm local regulations for electric watercraft on your preferred lakes or coastal areas, since some municipalities still classify them under traditional PWC rules despite the electric propulsion.

2. LightStream

LightStream operates as the online lending division of Truist Bank and focuses exclusively on unsecured personal loans for creditworthy borrowers. You won't need to pledge your boat as collateral, which speeds up approval and eliminates appraisal requirements. The lender funds recreational vehicle purchases including boats, jet skis, and sailboats through loans that close in as little as one business day after approval. If you have strong credit and want flexible financing without lien restrictions, LightStream delivers one of the fastest paths to low interest boat loans.

Best for

LightStream works best for borrowers with credit scores above 660 who want to avoid the documentation burden of secured marine financing. You keep full ownership of your watercraft from day one since the lender doesn't file a lien or require a marine survey. Buyers purchasing smaller vessels like Wave-Vo electric jet boats benefit most, since unsecured rates stay competitive up to $25,000 loan amounts before secured options become more cost-effective.

Typical APR range and loan terms

Rates start at 7.49% APR for the most qualified applicants and can reach 25.49% APR depending on your credit profile and loan duration. You can choose repayment terms from 24 to 144 months, though shorter terms always save you more in total interest. LightStream advertises a 0.50% rate discount if you set up automatic payments from a checking or savings account, which applies at funding and stays active throughout your loan term.

Loan amounts and what you can use the funds for

LightStream approves loans from $5,000 to $100,000, making it viable for everything from a $6,000 Wave-Vo to a mid-sized cabin cruiser. You can use the funds for new or used watercraft purchases, boat repairs, or marine equipment upgrades. The lender doesn't restrict how you spend the money as long as you declare the loan purpose at application.

Fees, prepayment rules, and rate discounts

You pay zero origination fees, no prepayment penalties, and no application charges. LightStream profits from interest alone, so paying off your balance early costs nothing extra. The automatic payment discount reduces your APR by half a percentage point, which saves $300 to $500 on a typical five-year boat loan.

"Unsecured loans eliminate the appraisal wait and collateral paperwork that delay traditional marine financing."

What you need to qualify

LightStream requires at least three years of credit history, stable income verification, and a debt-to-income ratio below 45%. You'll upload recent pay stubs or tax returns during the online application, and the system renders a decision within minutes for most applicants. Funding lands in your bank account as soon as the next business day after you accept the loan terms.

3. Navy Federal Credit Union

Navy Federal Credit Union ranks as the largest credit union in the United States by membership and consistently offers competitive marine financing rates for military-affiliated borrowers. The institution specializes in secured boat loans that use your watercraft as collateral, which allows them to offer lower APRs than most unsecured personal loan options. You'll face stricter documentation requirements compared to LightStream, but the rate savings add up significantly on larger loan amounts over long repayment periods.

Best for

Navy Federal works best for active duty military members, veterans, Department of Defense employees, and their immediate family members who need financing for boats valued above $25,000. The secured loan structure delivers the most savings when you're purchasing a vessel that requires a long repayment schedule. Borrowers with excellent credit scores and military service records qualify for the institution's lowest advertised rates, which can beat marketplace averages by one to two percentage points.

Typical APR range and loan terms

Rates start as low as 5.99% APR for the most qualified applicants and typically range up to 12.99% APR depending on your credit profile and loan term selection. You can choose repayment periods from 60 to 240 months, with longer terms available for higher-value vessels. Navy Federal adjusts rates based on whether you're buying new or used, the boat's age, and your down payment percentage.

New vs. used boat rules and collateral details

Navy Federal finances new boats without restrictions and used vessels up to 20 years old at the time of purchase. You'll need to provide the boat's hull identification number (HIN) and proof of value through a dealer invoice or marine survey. The lender files a lien on the title until you pay off the balance, which means you can't sell or transfer ownership without settling the loan first.

"Military-focused credit unions often deliver the most aggressive low interest boat loans for qualified service members and their families."

Membership and eligibility basics

You must join Navy Federal before applying for boat financing, which requires military affiliation through active service, veteran status, DoD employment, or family connection to an eligible member. Membership costs $5 to open a savings account, and approval happens instantly for most military personnel.

Fees, down payments, and how funding works

Navy Federal charges no origination fees or prepayment penalties on boat loans. You'll typically need to put down 10% to 20% of the purchase price, with larger down payments securing better rates. Funding arrives within five to seven business days after you submit all required documentation and complete the collateral verification process.

4. PenFed Credit Union

PenFed Credit Union competes directly with Navy Federal for military-affiliated boat financing but opens membership to a broader audience through community partnerships and employer sponsorships. The institution structures its low interest boat loans as secured financing that uses your watercraft as collateral, which delivers competitive rates for borrowers who qualify. You'll face similar documentation requirements as Navy Federal, including marine surveys and title verification, but PenFed's more accessible membership standards make it viable for civilian buyers who don't have direct military connections.

Best for

PenFed works best for creditworthy borrowers with scores above 650 who want secured boat loan rates without needing active duty military status. You'll benefit most if you're purchasing a vessel valued between $15,000 and $75,000 where the rate difference between secured and unsecured financing creates meaningful savings. Buyers planning shorter repayment terms of five to ten years maximize their interest savings since PenFed rewards faster payoff schedules with lower APRs.

Typical APR range and loan terms

Rates start at 6.24% APR for top-tier applicants and extend to 13.49% APR depending on your credit profile and loan duration. You can select repayment terms from 60 to 180 months, with rate discounts available for terms under 120 months. PenFed adjusts your rate based on the boat's age, purchase price, and whether you're refinancing an existing marine loan or financing a new purchase.

Boat types financed and lender restrictions

PenFed finances new and used boats up to 20 model years old at the time of purchase, including sailboats, fishing vessels, pontoons, and personal watercraft. The lender requires a minimum loan amount of $5,000 and caps individual borrowing at $500,000 for marine purchases. You cannot use PenFed boat loans for commercial fishing operations or charter businesses, and the watercraft must be titled in your name for personal recreational use.

"Credit unions with broader membership eligibility give you secured loan rates without military service requirements."

Membership and eligibility basics

You qualify for PenFed membership through military affiliation, employment at partner organizations, or by joining the National Military Family Association for a one-time $20 fee. Membership approval happens within 24 hours for most applicants, and you'll need to open a savings account with a $5 minimum deposit before applying for boat financing.

Fees, down payments, and payoff flexibility

PenFed charges zero origination fees and no prepayment penalties, letting you pay off your balance early without extra costs. You'll typically need a 10% to 15% down payment on boats over $25,000, with smaller down payments available for shorter loan terms. Funding completes within seven to ten business days after you submit required documentation including the marine survey and proof of insurance.

5. USAA

USAA provides marine financing exclusively for military members, veterans, and their families through a secured boat loan structure that uses your watercraft as collateral. The institution combines competitive interest rates with streamlined approval processes designed for military-affiliated borrowers who value straightforward terms and transparent pricing. You'll need to verify your military status during membership enrollment, but once approved, USAA delivers low interest boat loans with minimal fees and flexible repayment options that adapt to deployment schedules and military life transitions.

Best for

USAA works best for active duty personnel, veterans, and military spouses who want dedicated customer service teams familiar with military pay structures and deployment cycles. You'll benefit most if you're purchasing a mid-sized boat valued between $20,000 and $60,000 where secured loan rates deliver substantial savings compared to unsecured personal loans. Borrowers who anticipate overseas deployments or frequent relocations appreciate USAA's online account management and ability to adjust payment schedules during active service periods.

Typical APR range and loan terms

Rates start at 6.49% APR for the most qualified applicants and extend to 14.99% APR based on your credit score and loan structure. You can choose repayment terms from 60 to 180 months, with rate discounts available for shorter durations under 120 months. USAA adjusts your APR based on whether you're financing a new or used vessel, the boat's model year, and your down payment percentage.

How USAA boat financing works in 2026

USAA structures its boat loans as secured financing that requires a lien on your watercraft title until you complete repayment. You'll submit the boat's hull identification number and purchase documentation through the online portal, and USAA orders a marine survey for vessels over $50,000. The lender funds your loan by issuing a check directly to the seller or depositing funds into your USAA checking account for private party purchases.

Eligibility and membership requirements

You qualify for USAA membership through honorable military service, veteran status, or as an immediate family member of an eligible member. The institution verifies your military affiliation through Department of Defense records during the application process, which typically completes within one business day. You must establish a USAA membership before applying for boat financing.

"Military-focused lenders understand deployment schedules and offer payment flexibility that civilian banks rarely match."

Fees and steps to apply

USAA charges no origination fees and no prepayment penalties on marine loans. You'll need a 10% to 20% down payment on most boat purchases, with exact requirements varying by loan amount and creditworthiness. Funding completes within five to eight business days after you submit all required documentation including proof of insurance and title verification.

6. First Citizens Bank

First Citizens Bank operates as a regional lending institution with national reach that specializes in secured boat financing for borrowers who want relationship banking combined with competitive marine loan rates. The bank files a lien on your watercraft title and requires more detailed collateral verification than unsecured lenders, but this process delivers lower APRs for qualified buyers purchasing vessels above $30,000. You'll work directly with loan officers who understand marine financing specifics, and the bank structures its low interest boat loans to accommodate both new purchases and refinancing of existing marine debt.

Best for

First Citizens Bank serves established borrowers with credit scores above 680 who prefer working with traditional banks instead of credit unions or online lenders. You'll benefit most if you're purchasing a mid-to-large vessel valued between $35,000 and $150,000 where the secured loan structure creates substantial interest savings over unsecured alternatives. Buyers who value in-person service and local branch access appreciate First Citizens' physical presence in key coastal and lakefront markets across the southeastern and western United States.

Typical APR range and loan terms

Rates start at 6.99% APR for top-tier applicants and extend to 15.99% APR depending on your credit profile and loan duration. You can choose repayment terms from 60 to 180 months, with the bank offering rate discounts for shorter terms under 120 months. First Citizens adjusts your APR based on the boat's age, purchase price, and whether you establish a checking relationship with the institution before closing your marine loan.

Secured boat loan basics and collateral requirements

First Citizens requires a marine survey for vessels over $50,000 and uses your boat as collateral throughout the loan term. The bank files a perfected lien on your title, which means you cannot sell or transfer ownership until you satisfy the outstanding balance. You'll provide the hull identification number, proof of value, and title documentation during the application process.

"Regional banks combine traditional relationship service with competitive rates that online lenders struggle to match."

Down payment expectations and closing timeline

You'll typically need a 15% to 20% down payment on most boat purchases, with larger down payments securing better interest rates. First Citizens completes funding within 10 to 14 business days after you submit all required documentation and the marine survey clears their underwriting standards.

Fees and documents to prepare

First Citizens charges no origination fees but may assess a documentation fee of $50 to $150 at closing depending on your state. You'll need recent pay stubs, tax returns, proof of insurance, and the marine survey before the bank releases funds to the seller.

7. Boatbanker

Boatbanker operates as a marine loan broker rather than a direct lender, which means the platform connects you with multiple financing partners instead of underwriting loans itself. You submit one application through their system, and Boatbanker shops your profile to banks, credit unions, and specialty marine lenders in their network to find competitive offers. This broker model works best when you want to compare multiple low interest boat loans without triggering several hard credit inquiries, since Boatbanker's initial rate check uses a soft pull that doesn't impact your credit score.

Best for

Boatbanker serves borrowers shopping for rates across multiple lenders who want to avoid submitting separate applications to each institution. You'll benefit most if you have credit scores above 640 and need financing for boats valued between $25,000 and $500,000 where rate differences between lenders create substantial savings. Buyers purchasing from private sellers appreciate Boatbanker's ability to secure financing without requiring dealership relationships.

Typical APR range and loan terms

Rates through Boatbanker's network start at 6.49% APR for the most qualified applicants and extend to 16.99% APR depending on which lender ultimately funds your loan. You can access repayment terms from 60 to 240 months, with longer terms available for higher-value vessels. Your actual rate depends on your credit profile, the boat's age and value, and which lender in their network provides the best offer for your specific situation.

How broker-style boat financing works

You complete one application on Boatbanker's platform that includes your credit information, income verification, and boat purchase details. The system shares your profile with multiple lenders simultaneously, and you receive competing offers within 24 to 48 hours. You select the loan terms that work best for your budget, and Boatbanker coordinates the closing process with your chosen lender.

"Broker platforms let you compare offers from multiple institutions without submitting separate applications to each lender."

When it can beat dealership financing

Boatbanker often delivers better rates than dealer-arranged financing because you're accessing wholesale lending partnerships instead of retail markups. Dealers typically add 0.5% to 2% to your APR as compensation for arranging financing, while Boatbanker earns commission directly from lenders. You'll save more when dealers offer limited financing options or when your credit profile qualifies for lenders outside the dealership's normal network.

Fees, paperwork, and funding timeline

Boatbanker charges no application fees to borrowers, earning commission from the lenders in their network instead. You'll provide standard documentation including pay stubs, tax returns, and boat purchase information through their secure portal. Funding completes within seven to ten business days after you accept a loan offer and complete the lender's underwriting requirements.

8. Greater Texas Credit Union

Greater Texas Credit Union serves members across the Lone Star State with secured boat financing that combines regional pricing advantages with credit union member benefits. The institution focuses on Texas residents and workers who want competitive marine loan rates without national lender complexity. You'll access dedicated loan officers familiar with Texas lakes, coastal regulations, and regional boat dealerships, which streamlines approval for buyers purchasing watercraft in state. Greater Texas structures its low interest boat loans with flexible terms that accommodate both weekend recreational use and serious fishing equipment investments.

Best for

Greater Texas Credit Union works best for Texas residents with credit scores above 650 who want relationship banking through a regional institution. You'll benefit most if you're purchasing a boat valued between $15,000 and $75,000 where secured loan rates deliver meaningful savings compared to unsecured personal loans. Buyers who maintain checking accounts and other financial products with the credit union qualify for rate discounts and streamlined approval that reduce closing timelines.

Typical APR range and loan terms

Rates start at 6.74% APR for top-tier applicants and extend to 14.49% APR depending on your credit profile and loan structure. You can choose repayment terms from 60 to 180 months, with shorter terms under 120 months securing better interest rates. Greater Texas adjusts your APR based on the boat's age, purchase price, and whether you establish autopay from a Greater Texas checking account.

Membership and geographic considerations

You qualify for membership through Texas residency, employment in the state, or family connection to an existing member. The credit union requires proof of your Texas address through a driver's license or utility bill during enrollment. Membership costs $5 to open a savings account, and approval happens within one business day for most applicants.

"Regional credit unions deliver localized service that national lenders can't match for state-specific boat purchases."

Loan amount limits and boat eligibility rules

Greater Texas finances new and used boats up to 15 model years old at the time of purchase, with minimum loan amounts of $10,000 and maximum borrowing up to $250,000 for marine purchases. The credit union requires boats to be titled in Texas and used for personal recreation rather than commercial operations.

Fees, discounts, and application steps

Greater Texas charges no origination fees and no prepayment penalties on boat loans. You'll typically need a 15% to 20% down payment on vessels over $30,000, with rate discounts available when you set up automatic payments. Funding completes within seven to ten business days after you submit required documentation including proof of insurance and boat valuation.

9. South Carolina Federal Credit Union

South Carolina Federal Credit Union delivers regional marine financing for Palmetto State residents who want secured boat loans with competitive rates and member-focused service. The institution structures its financing as collateralized lending that uses your watercraft as security, which allows them to offer lower APRs than unsecured personal loan alternatives. You'll work with loan officers who understand South Carolina's coastal regulations and inland lake systems, and the credit union offers rate discount programs that reward long-term membership and automatic payment enrollment.

Best for

South Carolina Federal serves state residents with credit scores above 640 who want relationship banking through a community-focused institution. You'll benefit most if you're purchasing boats valued between $12,000 and $80,000 where secured loan rates create substantial savings over the loan term. Borrowers who maintain multiple accounts with the credit union qualify for preferential pricing that reduces their overall financing costs.

Typical APR range and loan terms

Rates start at 6.99% APR for the most qualified applicants and extend to 15.49% APR depending on your credit profile and repayment schedule. You can select terms from 60 to 180 months, with shorter durations under 120 months securing better interest rates. South Carolina Federal adjusts your APR based on the boat's age, value, and whether you've been a member for at least 12 months before applying.

Rate discount options to ask about

South Carolina Federal offers 0.25% to 0.50% APR reductions when you set up automatic payments from a credit union checking account. Members who maintain $10,000 or more in combined deposits may qualify for additional loyalty discounts that further reduce their low interest boat loans. Ask your loan officer about available promotions during your specific application period, since the credit union runs seasonal rate specials for marine financing.

"Regional credit unions reward member loyalty with rate discounts that national lenders rarely offer."

New vs. used boat restrictions

The credit union finances new boats without restrictions and used vessels up to 18 model years old at the time of purchase. You'll need a marine survey for boats over $40,000, and the lender requires title documentation showing clear ownership history.

Fees and how to apply

South Carolina Federal charges no origination fees and no prepayment penalties. You'll typically need a 10% to 15% down payment, and funding completes within seven to ten business days after document submission.

10. Space Coast Credit Union

Space Coast Credit Union specializes in extended-term marine financing that stretches repayment schedules up to 20 years for qualified borrowers purchasing higher-value vessels. The Florida-based institution structures its low interest boat loans as secured financing that uses your watercraft as collateral, which delivers competitive rates for buyers who need smaller monthly payments over longer periods. You'll trade lower monthly obligations for higher total interest costs compared to shorter loan terms, but this approach makes expensive boats more accessible if you prioritize cash flow management over lifetime savings.

Best for

Space Coast Credit Union serves Florida residents and workers with credit scores above 650 who want maximum payment flexibility through extended repayment schedules. You'll benefit most if you're purchasing a vessel valued between $40,000 and $200,000 where stretching payments over 15 to 20 years makes ownership feasible within your monthly budget. Borrowers who plan to keep their boats for decades and value predictable payment structures appreciate the stability that long-term fixed rates provide.

Typical APR range and loan terms

Rates start at 7.24% APR for top-tier applicants and extend to 16.49% APR depending on your credit profile and chosen loan duration. You can select repayment terms from 60 to 240 months, with the credit union offering their most aggressive low interest boat loans for terms under 180 months. Space Coast adjusts your APR based on the boat's age, purchase price, and your down payment percentage.

Long-term financing and total interest tradeoffs

A $75,000 boat financed at 8% APR over 20 years creates monthly payments around $627, but you'll pay roughly $75,000 in total interest over the loan lifetime. Compare that to a 10-year term on the same boat at the same rate, where monthly payments jump to $909 but total interest drops to approximately $34,000. You need to decide whether lower monthly obligations justify paying double or triple the interest cost over time.

"Extended loan terms create affordable monthly payments but dramatically increase your total financing cost."

Boat age, model year, and condition rules

Space Coast finances new boats without restrictions and used vessels up to 15 model years old at the time of purchase. The credit union requires a marine survey for all boats over $50,000 regardless of age, and you'll need documentation proving the vessel meets their condition standards for collateral purposes.

Fees, insurance requirements, and funding steps

Space Coast charges no origination fees and no prepayment penalties on marine loans. You'll need full coverage marine insurance throughout the loan term and a typical down payment of 15% to 20%. Funding completes within eight to twelve business days after you submit required documentation.

11. APGFCU

APGFCU (Aberdeen Proving Ground Federal Credit Union) serves military personnel, DoD employees, and defense contractors in the mid-Atlantic region with secured boat financing that prioritizes borrowers connected to the defense community. The Maryland-based institution structures its marine loans as collateralized financing that uses your watercraft as security, which delivers competitive rates for qualified members who meet their military or defense-sector employment requirements. You'll work with loan officers familiar with military pay schedules and security clearances, and the credit union adjusts loan terms to accommodate deployment cycles and government employment transitions.

Best for

APGFCU works best for military members, DoD civilians, and defense contractors stationed in Maryland, Virginia, or nearby states who want relationship banking through a defense-focused institution. You'll benefit most if you're purchasing boats valued between $10,000 and $60,000 where secured loan rates create meaningful savings. Borrowers who maintain checking accounts and direct deposit with the credit union qualify for preferential pricing that reduces overall financing costs.

Typical APR range and loan terms

Rates start at 7.49% APR for the most qualified applicants and extend to 15.99% APR depending on your credit profile and repayment duration. You can choose terms from 60 to 180 months, with shorter schedules under 120 months securing better interest rates. APGFCU adjusts your APR based on the boat's age, value, and your membership tenure with the institution.

Membership eligibility and service area

You qualify for membership through military service, DoD employment, or work with defense contractors affiliated with Aberdeen Proving Ground. The credit union also accepts family members of eligible individuals and residents in select Maryland counties. Membership requires a $5 savings account deposit and approval within one to two business days.

"Defense-focused credit unions understand military pay structures better than civilian lenders."

Loan amount tiers and how they affect rates

APGFCU finances boats from $5,000 to $100,000 with rate variations based on loan size. Loans under $25,000 receive simplified approval and faster funding, while amounts above $50,000 require marine surveys and extended underwriting. Your low interest boat loans rates improve when you borrow within the $15,000 to $50,000 range where the credit union offers their most competitive pricing.

Fees and required documentation

APGFCU charges no origination fees and no prepayment penalties. You'll need pay stubs, proof of insurance, and boat documentation during application. Funding completes within seven to ten business days after document submission.

12. Marcus by Goldman Sachs

Marcus by Goldman Sachs operates as the consumer banking arm of Goldman Sachs and offers unsecured personal loans that borrowers frequently use for boat purchases. The platform doesn't market marine-specific financing, but you can apply loan proceeds toward watercraft purchases without collateral restrictions or lien filings. Marcus delivers fast approval and funding compared to traditional boat lenders, making it viable for smaller vessel purchases like Wave-Vo electric jet boats where unsecured rates stay competitive with secured alternatives.

Best for

Marcus works best for borrowers with credit scores above 660 who want to avoid the documentation burden of secured marine financing. You'll benefit most when purchasing boats valued under $25,000 where the APR difference between unsecured and secured loans creates minimal cost impact over shorter repayment periods. Buyers who value speed and simplicity over the lowest possible rate appreciate Marcus's streamlined approval process.

Typical APR range and loan terms

Rates start at 7.99% APR for the most qualified applicants and extend to 24.99% APR depending on your credit profile and chosen loan duration. You can select repayment terms from 36 to 72 months, with shorter terms securing better interest rates. Marcus provides fixed rates that never change throughout your loan term, which protects you from market fluctuations.

When an unsecured personal loan makes sense for a boat

Unsecured loans eliminate the marine survey requirements, title verification, and lien filing processes that secured boat financing demands. You'll save two to three weeks in closing time and keep full ownership rights from day one. This approach works when you're buying a smaller watercraft where the APR premium costs less than $500 to $1,000 in additional interest compared to secured alternatives.

How to compare APR vs. secured boat loans

Calculate your total interest cost on a $15,000 boat at 9% APR over five years versus a secured loan at 7% APR over the same term. The unsecured option costs approximately $3,728 in interest while the secured version costs around $2,800. That $928 difference may justify paying more for the convenience and speed of Marcus's unsecured structure.

"Unsecured personal loans trade slightly higher rates for dramatically faster funding and zero collateral hassles."

Fees, prepayment rules, and funding speed

Marcus charges no origination fees, no prepayment penalties, and no application costs. You can pay off your balance early without extra charges. Funding arrives within one to three business days after you accept loan terms, making it the fastest option in this guide.

Next steps

You now have 12 vetted lenders offering competitive low interest boat loans in 2026, each with distinct advantages for different buyer profiles. Start by checking your credit score to determine which lenders will offer you their best rates, then request quotes from three to five institutions that match your boat purchase price and desired loan term. Compare the total interest cost over the full repayment period, not just monthly payments, since longer terms dramatically inflate what you'll ultimately spend.

Before you commit to a loan, consider whether you actually need traditional marine financing at all. Wave-Vo's electric jet boats start at $6,000, which puts ownership within reach of a simple personal loan or even cash savings. You'll skip the trailer, fuel costs, and maintenance expenses that push traditional boats into five-figure financing territory. Explore Wave-Vo's electric jet boats to see if eliminating the boat loan entirely makes more sense than shopping for the lowest rate.